According to new research, over the space of six years SME lending has decreased by £2.6 billion… .

<

div>According to new research, over the space of six years SME lending has decreased by £2.6 billion.

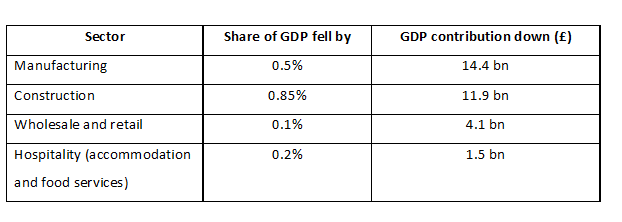

In key sectors such as retail trade, construction and hospitality, the relative contribution to overall GDP of those sectors has seen stronger decline than in other sectors between the pre-recession year 2007 and 2013. At the same time, lending to SMEs in the UK has contracted by £2.6 billion (£41.8 billion in 2008 to £39.2 billion in 2012)

Marc Glazer, CEO of Boost Capital, stressed: “The real contribution and value to the nation’s economy from SMEs should never be understated. Big sectors dominated by SMEs, like hospitality and construction, have shown comparatively lower growth than other sectors. If funding for these businesses continues to be constrained, their growth and ultimate contribution to Britain’s bottom line may fall far below its potential.”

“The stunted growth, often in sectors with large numbers of SMEs, could be caused by numerous reasons given the incredibly bumpy ride for the UK economy in the last seven years. Mostly, from what we have seen on the ground at Boost Capital, SMEs are still not being given the financial footpaths to grow.”

These findings are further underlined by data from government analysis on bank lending to SMEs which found that the size of a firm is a significant factor in a loan or overdraft application being rejected. The smaller the firm, the more likely they are to be rejected.

The emerging industry of ‘alternative lenders’ is making headway by offering businesses across virtually any sector, viable options to fund their growth. However, as discussed in the Treasury Select Committee session, there are still too many SMEs not even applying as they don’t know about their options or assume they won’t qualify. Boost Capital, an alternative lender in the UK market, has a lending model designed specifically for SMEs that takes into account their unique requirements. At the heart of the model is a balance of providing quick access to capital without the repayments putting a financial strain on cash flow so the business can grow.

Boost Capital has been trading in the US market with parent company, Business Financial Services for over 10 years and has seen a similar situation to the UK with SME lending in the US down by 17 per cent ($56 billion - £33 billion equivalent) since 20085. The US also shows a similar trend with SME dominated sectors underperforming relative to those with a greater proportion of large businesses.

Glazer continued, “In the US, we’ve witnessed a double impact since starting out as an alternative lender. On the one hand, the percentage of small business loans in bank portfolios has dropped from 51 per cent in 1998 to 36 per cent in 2008 and even lower to 29 per cent in 2012.5 On the other,18 per cent of SMEs did not even attempt to apply as they did not believe they would be approved.

“In the UK, we’ve seen very similar trends in funding supply and demand since our launch in 2012. But, we have also seen some very encouraging signs from the Government to tackle this impact as they push towards a referral system. Businesses declined by traditional lenders can seek an alternative option which may suit their needs better in the long run.”

Boost Capital meets SME funding needs quickly to help them grab opportunities which might otherwise slip through their fingers. A small business will know within 24 hours if they are approved and can have access to the capital they need within as few as two days.

Examples of SME dominated sectors that have seen particular reductions in their contributions since 2007, include hospitality, construction, wholesale and retail, and manufacturing.

Leave a comment