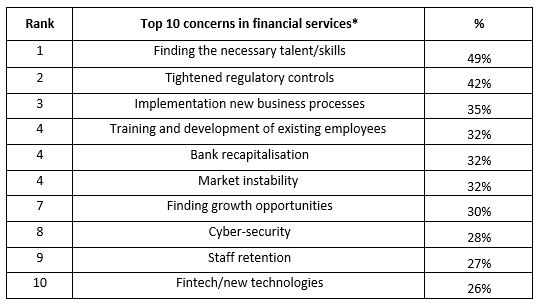

A survey conducted by Robert Half Financial Services – which highlighted the key concerns facing the industry – found that tightened regulatory controls (42%), new business processes (35%), and training and development for employees (32%) were the other major worries for respondents.

Matt Weston, UK managing director at Robert Half (pictured above), said that process, regulatory and geopolitical changes were creating the perfect storm for the financial services sector to develop and grow.

- Is the bridging market facing a skills crisis?

- SMEs across the world suffer from skills shortages

- Nucleus Commercial Finance launches apprenticeship product

“In a time of uncertainty, banks and other financial services firms need to be confident they can access the skills they need to help them through this current period of change and beyond.”

The survey also revealed that new technologies, such as blockchain and automation, were less of a worry, with only 13% and 6% respectively fearing their impact.

Matt added: “With only a finite number of skilled professionals, providing current staff with the means to grow and develop new skills provides tangible benefits to the business as a whole, including plugging skills gaps.

“Staff provided with such opportunities are more motivated, productive and loyal, which has a positive impact on any organisation.

“Additionally, while operating in a period of change or market instability, adopting a flexible recruitment strategy can offer great benefits.

“Where current skills gaps do exist, hiring in temporary or contract professionals to fill those gaps allows for added value, greater flexibility and controls.”

Leave a comment